Jobs Day • Stocks Rebound • REIT Dividend Hikes & Cuts

U.S. equity markets rebounded Friday following four-straight days of declines after a solid jobs report and a recovery in several beaten-down regional banks calmed market jitters and recession concerns.

Paring its weekly declines to under 1%, the S&P 500 rallied 1.9% today, while the Mid-Cap 400 and Small-Cap 600 each gained more than 2%. The Dow jumped 547 points.

Real estate equities finished broadly higher as well today as a relatively strong earnings season winds down. The Equity REIT Index advanced 1.7% today with 17-of-18 property sectors in positive-territory.

Arbor Realty (ABR) rallied after reporting strong results and raising its dividend by 5% to $0.42/share (15.4% dividend yield), the fourth mortgage REIT to raise its dividend this year - and 48th REIT in total.

Cold storage operator Americold (COLD) rallied 5% after reporting strong results and significantly raising its full-year outlook. A pair of REITs trimmed their dividends - City Office (CIO) reduced its dividend by 50% while Great Ajax (AJX) trimmed its dividend by 20%.

Income Builder Daily Recap

U.S. equity markets rebounded Friday following four-straight days of declines after a solid jobs report and a recovery in several beaten-down regional banks calmed market jitters and recession concerns. Paring its weekly declines to under 1%, the S&P 500 rallied 1.9% today, while the Mid-Cap 400 and Small-Cap 600 each gained more than 2%. The Dow jumped 547 points. Benchmark interest rates rebounded from nine-month lows with the 2-Year Treasury Yield climbing 9 basis points to 3.89% while the 10-Year Treasury Yield climbed 9 basis points to 3.45%. Real estate equities finished broadly higher as well today as a relatively strong earnings season winds down. The Equity REIT Index advanced 1.7% today with 17-of-18 property sectors in positive territory, while the Mortgage REIT Index rebounded 3.0%.

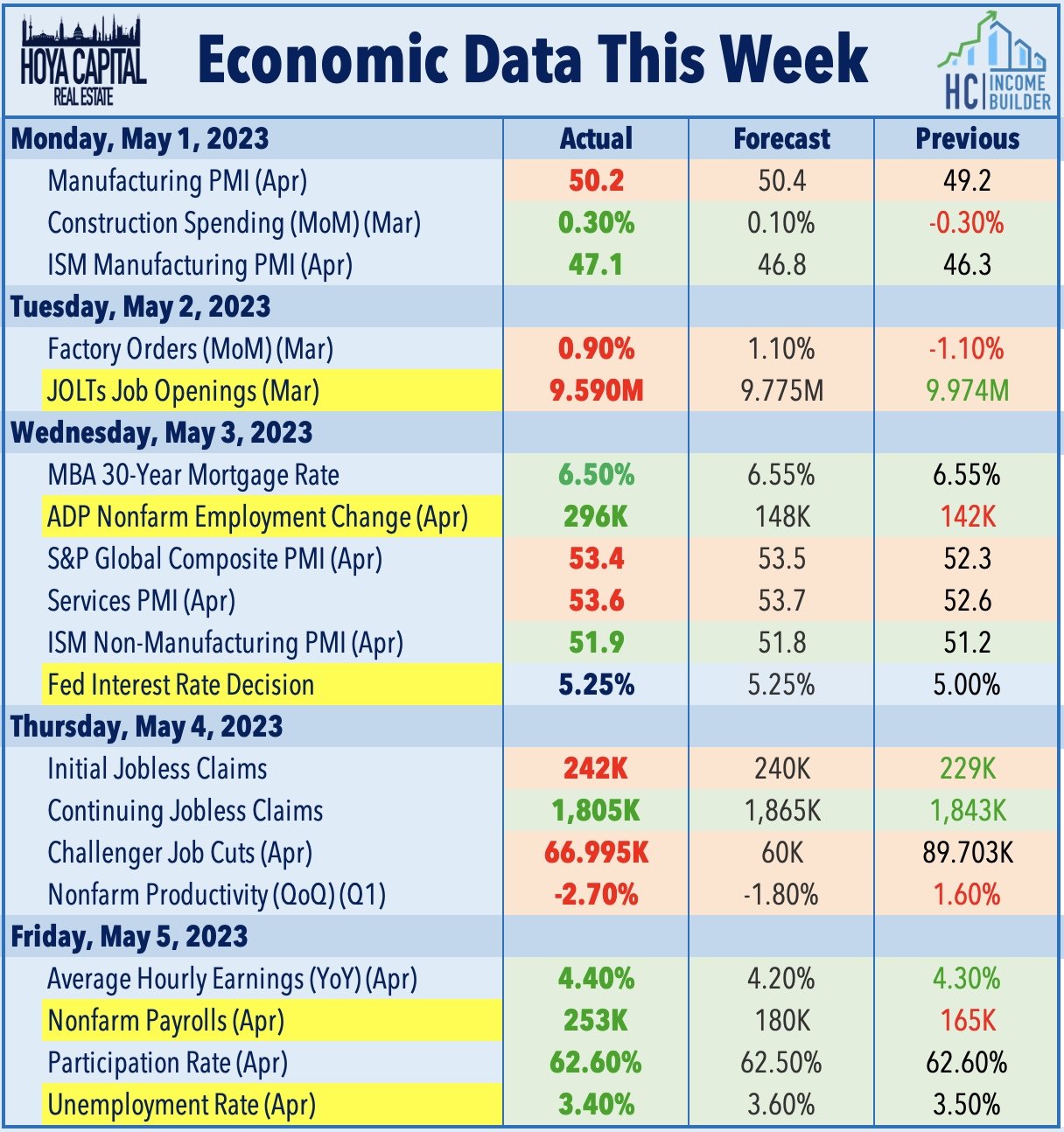

The critical BLS nonfarm payrolls report this morning showed that the U.S. economy added 253k jobs in April - above expectations of 180k - which marked a modest reacceleration from a downwardly-revised March and February. Earlier in the week, ADP Research reported that private payrolls rose 296k, which was also well above the median estimate of 145k. The most relevant inflation-related metric in determining the path of Fed policy - Average Hourly Earnings - was slightly hotter-than-expected, rising at a 4.4% annual rate, which was above the forecast of 4.2% Perhaps skewing these numbers on the upside, however, job gains in April were particularly strong in higher-wage industries with the professional services and healthcare categories accounting or nearly half of the job gains, while hiring in the retail, hospitality, and temporary help categories has trended lower in recent months.

Real Estate Daily Recap

Best & Worst Performance Today Across the REIT Sector

Industrial: Cold storage operator Americold (COLD) rallied 5% after reporting strong results and significantly raising its full-year outlook. Driven by a significant rebound in occupancy rates due to improved staffing conditions at food distributors, COLD now expects to report full-year same-store NOI growth of 14.5% - up from its prior outlook of 6.6% growth - and raised its full-year FFO target to 9.0% - up 180 basis points from last quarter. Today, we published Industrial REITs: We Love Logistics. After the worst year of performance on record in 2022, Industrial REITs have rebounded this year after earnings results showed a surprising re-strengthening of property-level fundamentals. Recent earnings results showed that demand continues to substantially outpace available supply. Rent growth reaccelerated in Q1, with rental spreads averaging over 40%, while occupancy rates climbed to fresh record highs. As noted in the report, strengthening rent growth comes despite substantial downward pricing power across other areas of the supply chain.

Net Lease: Agree Realty (ADC) gained about 1% after reporting in-line results and raising its full-year acquisitions target from $1 billion to $1.2 billion. ADC noted that it acquired 95 properties in Q1 for $314 million at a weighted average cap rate of 6.7% - the lowest cap rate of any net lease REIT this earnings season. The 6.7% cap rate was 70 basis points above its average from Q1 2022, a time when benchmark interest rates were roughly 200 basis points below today's levels. ADC observed a "lack of competition amongst both public and private buyers" at the prices it was willing to pay. Results from most of the other major net lease REITs showed more significant upward movement in cap rates. Realty Income (O) reported a 130 basis point increase in cap rates from last year while both Spirit Realty (SRC) and Broadstone (BNL) transacted at a cap rate that was 150 basis points higher.

Strip Center: A trio of strip center REITs rounded out a relatively strong earnings season for the strip center sector in which roughly half the sector raised their full-year FFO outlook. Regency Centers (REG) gained 1% after reporting strong results and raising its full-year NOI and FFO guidance. REG now expects NOI growth of 3.0% this year - up 50 basis points from last quarter - and sees its FFO increasing 0.2% - an improvement from its prior outlook calling for a 0.7% decline. Rent spreads cooled a bit in Q1, however, with cash leasing spreads increasing 5.5% in Q1 - the weakest since Q3 of 2021. Federal Realty (FRT) finished roughly flat after it maintained its full-year outlook but noted that its cash leasing spreads accelerated to 11.0% in Q1, its strongest quarter since Q2 2020. Small-cap Saul Centers (BFS) - which does not provide guidance - dipped 5% after reporting mixed results.

Mortgage REIT Daily Recap

Mortgage REITs rebounded today following sharp declines over the prior several sessions. Arbor Realty (ABR) - which we own in the Focused Income Portfolio - rallied after reporting adjusted EPS of $0.62 - above consensus estimates of $0.50 - and raised its dividend by 5% to $0.42/share (15.4% dividend yield), the fourth mortgage REIT to raise its dividend this year. In the earnings call, ABR pushed back strongly on the claims of a contingent of short-sellers that have targeted the firm in recent quarters with "false and misleading information cloaked in the form of opinion." ABR noted that it saw no increases in default to delinquencies in the first quarter and that the debt restructuring of a Houston loan portfolio - a focus of the short report - was completed with no losses on the original debt and the recovery of all the outstanding interest. Western Asset (WMC) rallied 4% after reporting that its Book Value Per Share ("BVPS") rose 5% in Q1 - the best among the mREITs to report results thus far. AG Mortgage (MITT) rallied 7% after it reported that its BVPS rose 4% in Q1 - the second-strongest in the sector. Great Ajax (AJX) slid 6% after reporting weaker-than-expected results, including a 3% decline in its BVPS to $12.58/share, and trimming its dividend by 20% to $0.20/share (13.5% dividend yield)

Economic Data This Week

We'll publish a full analysis and commentary of this week's developments in the real estate industry, as well as an analysis of the busy week of economic data in our Real Estate Weekly Outlook this weekend.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds ("ETFs") listed on the NYSE. In addition to any long positions listed, Hoya Capital is long all components in the Hoya Capital Housing Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital Research & Index Innovations (“Hoya Capital”) is an affiliate of Hoya Capital Real Estate, a registered investment advisory firm based in Rowayton, Connecticut that provides investment advisory services to ETFs, individuals, and institutions. Hoya Capital Research & Index Innovations provides non-advisory services including market commentary, research, and index administration focused on publicly traded securities in the real estate industry.

This published commentary is for informational and educational purposes only. Nothing on this site nor any commentary published by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. This commentary is impersonal and should not be considered a recommendation that any particular security, portfolio of securities, or investment strategy is suitable for any specific individual, nor should it be viewed as a solicitation or offer for any advisory service offered by Hoya Capital Real Estate. Please consult with your investment, tax, or legal adviser regarding your individual circumstances before investing.

The views and opinions in all published commentary are as of the date of publication and are subject to change without notice. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Any market data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any outlook made in this commentary will be realized.

Readers should understand that investing involves risk and loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks, as do investments in ETFs. The information presented does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes.

Hoya Capital Real Estate and Hoya Capital Research & Index Innovations have no business relationship with any company discussed or mentioned and never receives compensation from any company discussed or mentioned. Hoya Capital Real Estate, its affiliates, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings and additional important disclosures is available at www.HoyaCapital.com.