Inflation Cools • Prologis Earnings • Apartment M&A

- U.S. equity markets finished broadly lower Wednesday despite encouraging inflation and housing market data as investors parsed commentary from Fed officials who reiterated calls for additional interest-rate increases.

- Following modest declines on Tuesday, the S&P 500 dipped 1.6% today while the tech-heavy Nasdaq 100 fell 1.3% - snapping a seven-day rally. The 10-Year Treasury Yield dipped to four-month-lows.

- Despite a strong start to REIT earnings season, real estate equities were also under pressure today with the Equity REIT Index slipping 1.5% with 17-of-18 property sectors in negative territory.

- Prologis (PLD) kicked-off REIT earnings season with very strong results, noting that it expects Core FFO growth of nearly 10% in 2023. After the close today, Veris Residential (VRE) announced that it will not proceed with a proposed takeover offer from Kushner Companies.

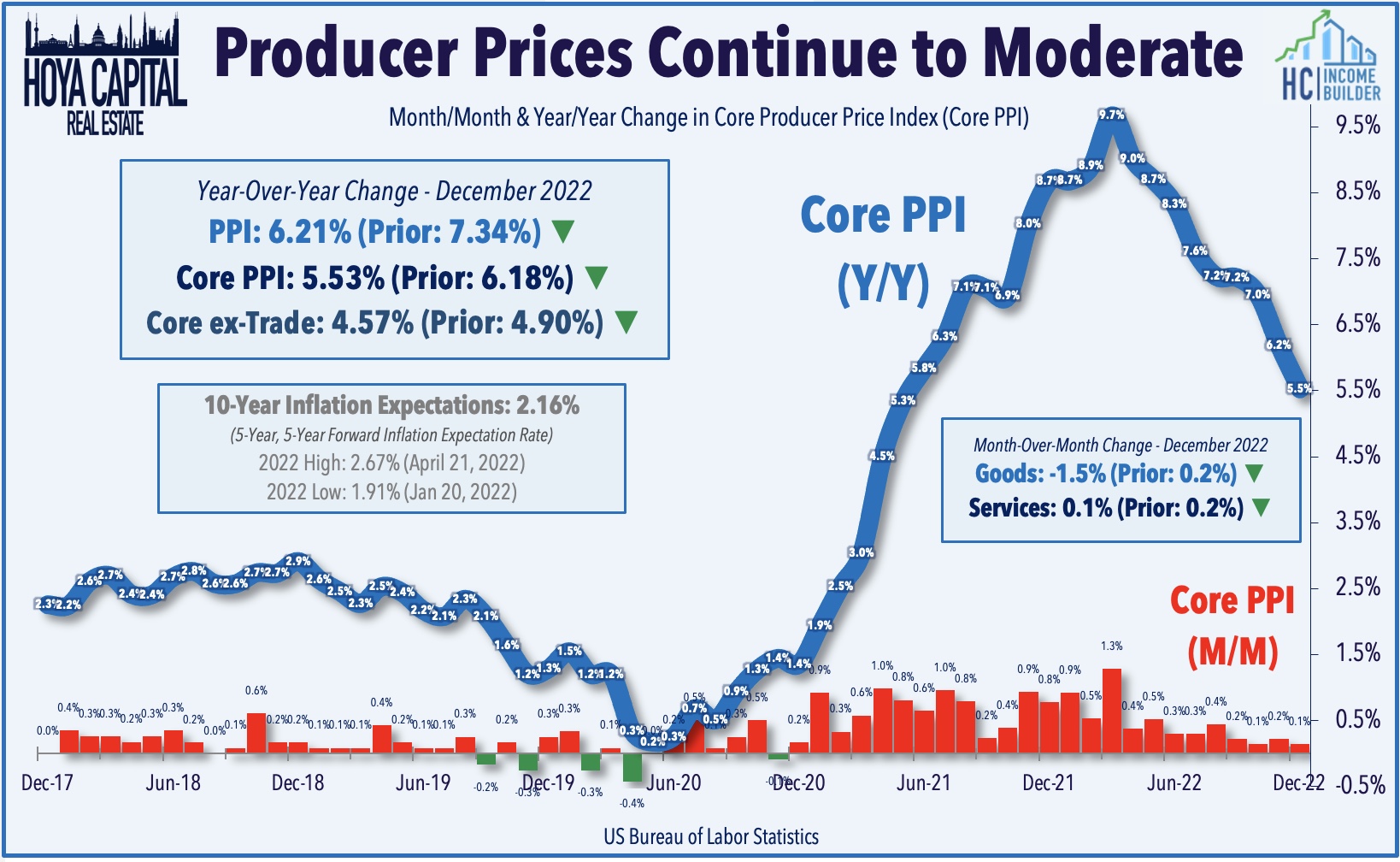

- Following the cooler-than-expected CPI report last week, investors saw another encouraging sign that inflationary pressures have eased with Producer Price Index data this morning showing that wholesale prices fell sharply in December.

Income Builder Daily Recap

U.S. equity markets finished broadly lower Wednesday despite encouraging inflation and housing market data as investors parsed commentary from Fed officials who reiterated calls for additional interest-rate increases. Following modest declines on Tuesday, the S&P 500 dipped 1.6% today while the tech-heavy Nasdaq 100 fell 1.3% - snapping a seven-day rally. Despite a strong start to REIT earnings season, real estate equities were also under pressure today with the Equity REIT Index slipping 1.5% with 17-of-18 property sectors in negative territory while the Mortgage REIT Index slipped 0.3%.

Despite the hawkish Fed commentary, bonds rallied today after a busy slate of economic data this morning showed a continued softening of economic conditions in December. The 10-Year Treasury Yield dipped 16 basis points to close at 3.38% today - the lowest since early September. Crude Oil prices dipped 2%, snapping an eight-day streak of gains. All eleven GICS equity sectors were lower today, but homebuilders and the broader Hoya Capital Housing Index were among the upside standouts on data showing a rebound in housing demand amid a retreat in mortgage rates with mortgage demand and homebuilder sentiment each rebounding in early 2023.

Following the cooler-than-expected CPI report last week, investors saw another encouraging sign that inflationary pressures have eased with Producer Price Index data this morning showing that wholesale prices fell sharply in December. The headline PPI Index declined 0.5% for the month - a sharper decline than the 0.1% consensus forecast - which dragged the annual increase to 6.2%, the lowest annual level since March 2021 and down considerably from the 10% annual increase in 2021. Notably, the PPI Goods Index dipped 1.5% in the month - helped by a 7.9% plunge in energy prices and a 1.2% decline in food prices. The PPI Services Index increased by 0.1%, pulling the annual increase down to 5.0% - the lowest since early 2021.

Retailers were under pressure today following disappointing Retail Sales data for the critical holiday month of December. Retail sales were higher by 6.0% on a year-over-year basis in December - the lowest annual increase since December 2020 and below the CPI Index during that period which rose 6.5%. On a month-over-month basis, seasonally-adjusted sales were lower by 1.1% in December - worse than the 0.8% decline expected - as a sharp decline in spending at department stores was partially offset by relatively strong spending at home improvement stores and grocery stores. Online sales declined 1.1% for the month but were still nearly 14% above 2021 levels.

Real Estate Daily Recap

Best & Worst Performance Today Across the REIT Sector

Industrial: Prologis (PLD) - which we own in REIT Dividend Growth Portfolio - gained 1% today after kicking off REIT earnings season with very strong results, reporting that its full-year Core FFO rose 11.1% in 2022 and provided initial 2023 guidance calling for Core FFO growth of 9.5%. Prologis recorded net effective rent growth of 50.6% in Q4 (down slightly from record-highs of 59.7% in Q3) and cash rent growth of 32.4% (also down from record-highs of 38.5% in Q3). Today we published Industrial REITs: Shortages Become Gluts which discussed the outlook for the logistics property sector heading into 2023 amid concerns over the "boom-bust" dynamics seen in pricing power across other segments of global supply chains including shipping and trucking. Industrial REITs aren't entirely immune from post-pandemic demand normalization, but supply remained inherently capped by land constraints. Rent growth will naturally moderate toward "trend" levels, but fundamentals are forecast to remain healthy absent a demand shock.

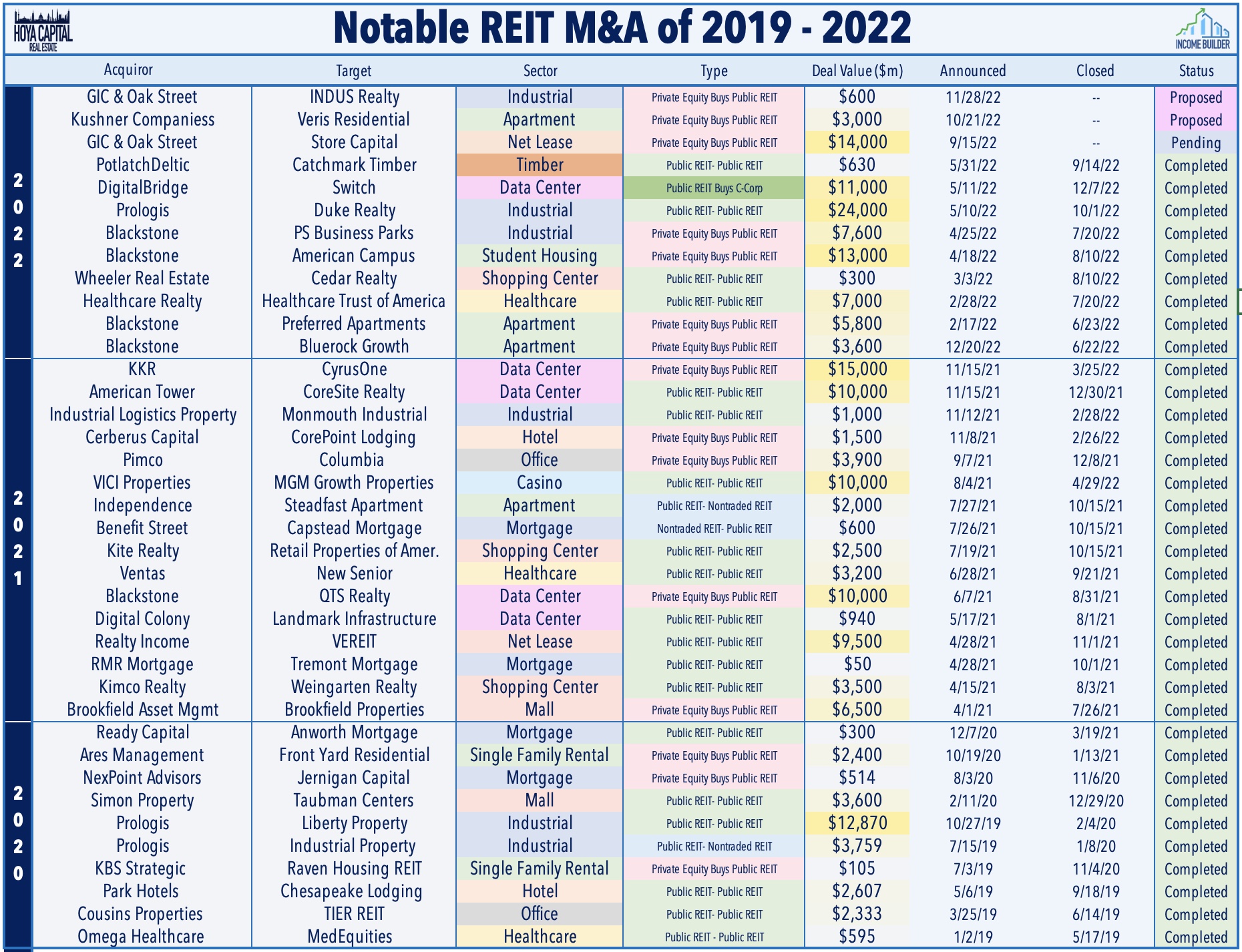

Apartments: After the close today, Veris Residential (VRE) announced that it will not proceed with a proposed takeover offer from Kushner Companies to buy the REIT at $18.50/share. Speaking of M&A activity, Nareit published a report today which recapped the busy year of M&A activity across the REIT sector in 2022. Total REIT merger and acquisition (M&A) activity came to $83.0 billion in 2022, the second highest annual figure since 2007, with transactions taking place across a range of property sectors. Total public-to-public REIT M&A in 2022 was $69.2 billion - comprising 83% of total REIT M&A activity - with the remaining 17% representing public-to-private deals. Prologis' acquisition of Duke Realty stood out as the largest transaction of 2022, with a value of $25.4 billion. Blackstone was also a major player in 2022, with deals that included the purchase of four public REITs - American Campus, Preferred Apartments, Bluerock Growth, and PS Business Parks.

Additional Headlines from The Daily REITBeat on Income Builder

- Moody’s affirmed the “Baa3” issuer rating and “Baa3” senior unsecured debt rating of Corporate Office Properties (OFC) with a stable outlook

- Moody’s affirmed the “Baa1” senior unsecured debt and “Baa2” preferred stock ratings of Kimco (KIM) with a stable outlook

- Hoya Capital High Dividend Yield ETF (RIET) declared a monthly distribution of $0.0855 per share, an increase of 2.4% over the previous monthly dividend.

- Hoya Capital Housing ETF (HOMZ) declared a monthly distribution of $0.0675 per share, an increase of 12.5% over the previous monthly dividend.

Mortgage REIT Daily Recap

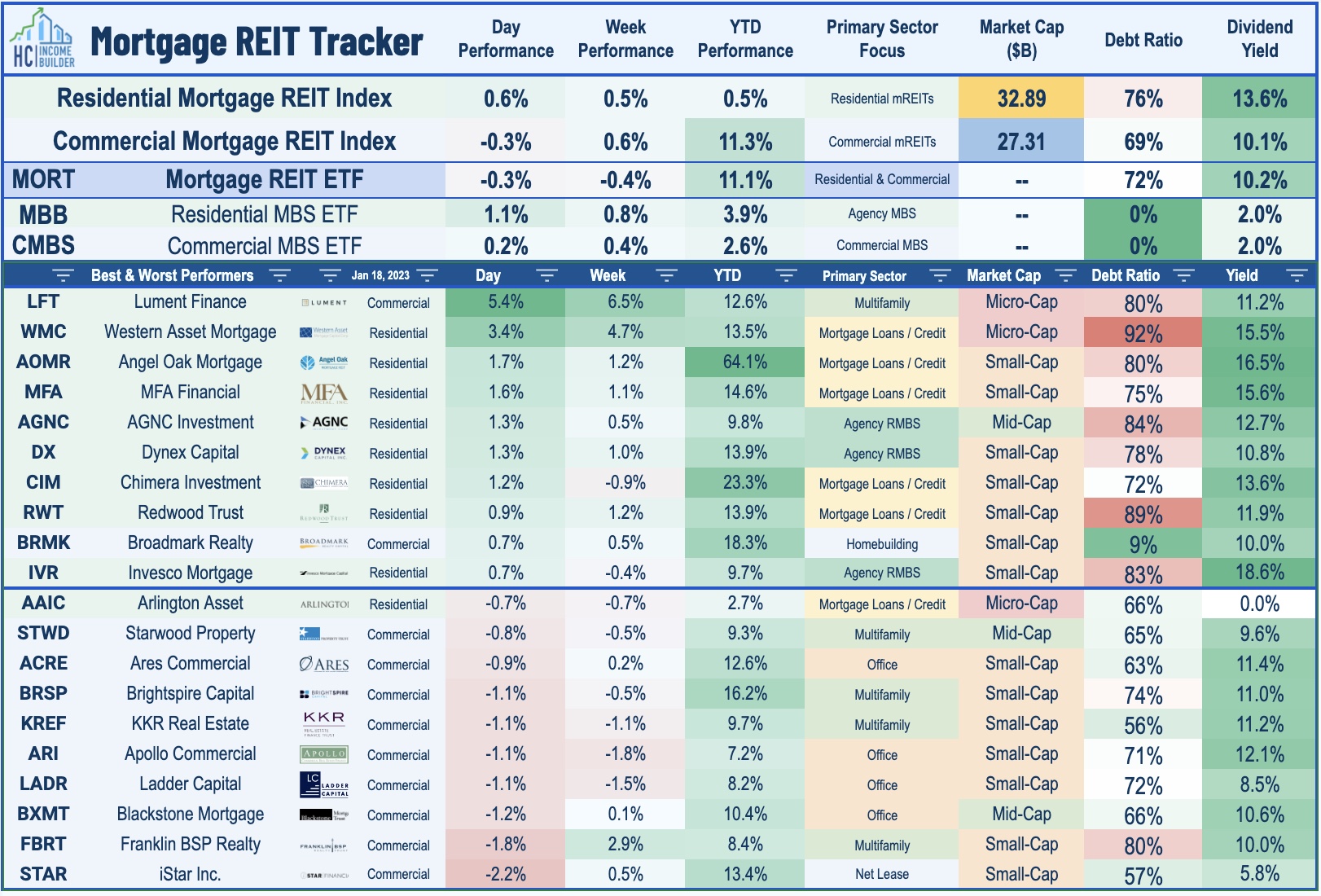

Per the REIT Rankings Tracker available to Income Builder subscribers, mortgage REITs were mixed today with residential mREITs gaining 0.6% while commercial mREITs slipped 0.3%. Broadmark Realty (BRMK) gained about 1% after holding its monthly dividend steady at $0.035/share, representing a forward dividend yield of 10.07%. BRMK was one of three commercial markets to lower its dividend in 2022, however, having paid a rate of $0.07 last January. Last month, we published Mortgage REITs: High Yields Are Fine, For Now, which noted that despite paying average dividend yields in the mid-teens, the majority of mREITs have been able to cover their dividends, but we flagged a handful of mREITs with payout ratios above 100% of EPS.

Economic Data This Week

The state of the U.S. housing market is in the spotlight in another jam-packed week of economic data. Markets will be closed on Monday in observance of Martin Luther King Day. Today, we saw NAHB Homebuilder Sentiment data for January along with Retail Sales data for the critical December holiday period and the Producer Price Index. On Thursday, we'll see Housing Starts and Building Permits data which is expected to show a further pull-back in home construction activity to levels below that of late 2019. On Friday, Existing Home Sales data is expected to dip below a 4 million-unit annualized rate for the first time since August 2010 - which is currently the only month in the past quarter century with a sales rate below 4 million.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital Research & Index Innovations (“Hoya Capital”) is an affiliate of Hoya Capital Real Estate, a registered investment advisory firm based in Rowayton, Connecticut that provides investment advisory services to ETFs, individuals, and institutions. Hoya Capital Research & Index Innovations provides non-advisory services including market commentary, research, and index administration focused on publicly traded securities in the real estate industry.

This published commentary is for informational and educational purposes only. Nothing on this site nor any commentary published by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. This commentary is impersonal and should not be considered a recommendation that any particular security, portfolio of securities, or investment strategy is suitable for any specific individual, nor should it be viewed as a solicitation or offer for any advisory service offered by Hoya Capital Real Estate. Please consult with your investment, tax, or legal adviser regarding your individual circumstances before investing.

The views and opinions in all published commentary are as of the date of publication and are subject to change without notice. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Any market data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any outlook made in this commentary will be realized.

Readers should understand that investing involves risk and loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks, as do investments in ETFs. The information presented does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes.

Hoya Capital Real Estate and Hoya Capital Research & Index Innovations have no business relationship with any company discussed or mentioned and never receives compensation from any company discussed or mentioned. Hoya Capital Real Estate, its affiliates, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings and additional important disclosures is available at www.HoyaCapital.com.