Inflation Week • Return To Office? • Storage In Focus

U.S. equity markets rebounded Monday following their worst week since April as bond markets stabilized ahead of another busy week of corporate earnings results and the critical CPI and PPI inflation reports.

Snapping a four-day losing streak, the S&P 500 advanced 0.9%, while the Dow Jones Industrial Average gained 408 points.

Real estate equities were among the leaders today ahead of the final stretch of earnings season over the next several days. Led by office and self-storage REITs, the Equity REIT Index advanced 1.3% today

Several of the most beaten-down coastal office REITs rallied today after tech-firm Zoom - a company that has been the "poster child" of the Work from Home Era - made a splash by calling its employees back to the office.

The Wall Street Journal published an in-depth column on the state of the self-storage industry this morning which focused, in part, on the remarkably strong performance of the industry since the start of the pandemic.

Income Builder Daily Recap

U.S. equity markets rebounded Monday following their worst week since April as bond markets stabilized ahead of another busy week of corporate earnings results and the critical CPI and PPI inflation reports. Snapping a four-day losing streak, the S&P 500 advanced 0.9%, while the Dow Jones Industrial Average gained 408 points. Mid-caps and Small-Caps posted more muted advances following notable outperformance last week. Real estate equities were among the leaders today ahead of the final stretch of earnings season over the next several days. Led by office and self-storage REITs, the Equity REIT Index advanced 1.3% today, with 17-of-18 property sectors finishing in positive territory, while the Mortgage REIT Index slipped 0.1%.

Inflation data is in the spotlight in another jam-packed week of economic data in the week ahead. The main event comes on Thursday with the Consumer Price Index for July, which investors and the Fed are hoping will show a continued cooling of inflationary pressures. The headline CPI is expected to moderate to a 2.8% year-over-year rate as some of the "hottest" prints seen in mid-2022 begin to roll off. We've noted in recent reports that "real-time" inflation - as measured by the CPI-ex-Shelter Index - has averaged less than 1% since last July. We speculate that an inevitable "2-handle" on the headline CPI will be a key narrative-shifting threshold for even the most hawkish Fed officials. On Friday, we'll see the Producer Price Index, which is expected to show an even more significant cooling of price pressures, with the headline PPI expected to slow to just a 0.7% year-over-year rate - down from the recent peak last March at 11.8%. On Friday, we'll see get the first look at Michigan Consumer Sentiment for August - a report which includes the closely-watched inflation expectations survey.

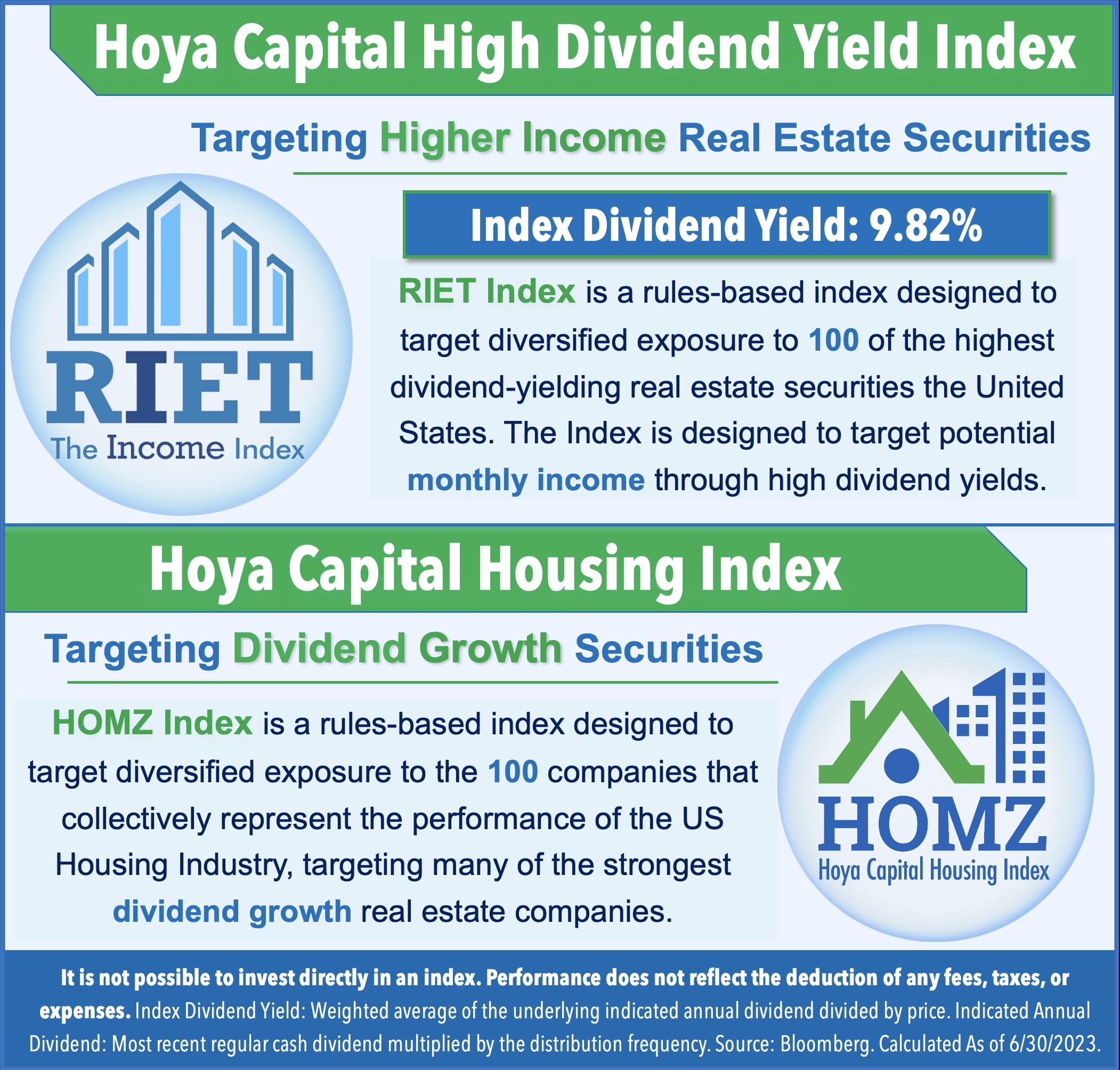

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds ("ETFs") listed on the NYSE. In addition to any long positions listed, Hoya Capital is long all components in the Hoya Capital Housing Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital Research & Index Innovations (“Hoya Capital”) is an affiliate of Hoya Capital Real Estate, a registered investment advisory firm based in Rowayton, Connecticut that provides investment advisory services to ETFs, individuals, and institutions. Hoya Capital Research & Index Innovations provides non-advisory services including market commentary, research, and index administration focused on publicly traded securities in the real estate industry.

This published commentary is for informational and educational purposes only. Nothing on this site nor any commentary published by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. This commentary is impersonal and should not be considered a recommendation that any particular security, portfolio of securities, or investment strategy is suitable for any specific individual, nor should it be viewed as a solicitation or offer for any advisory service offered by Hoya Capital Real Estate. Please consult with your investment, tax, or legal adviser regarding your individual circumstances before investing.

The views and opinions in all published commentary are as of the date of publication and are subject to change without notice. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Any market data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any outlook made in this commentary will be realized.

Readers should understand that investing involves risk and loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks, as do investments in ETFs. The information presented does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes.

Hoya Capital Real Estate and Hoya Capital Research & Index Innovations have no business relationship with any company discussed or mentioned and never receives compensation from any company discussed or mentioned. Hoya Capital Real Estate, its affiliates, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings and additional important disclosures is available at www.HoyaCapital.com.