Yields Dip • Housing Rebounds • REIT Dividends

- U.S. equity markets finished lower for a fifth-day Wednesday even as long-term interest rates dipped to three-month lows as investors weighed recession worries against encouraging news on the inflation front.

- Extending its declines to nearly 3.5% on the week, the S&P 500 dipped another 0.2% today while the Nasdaq 100 declined 0.4%.

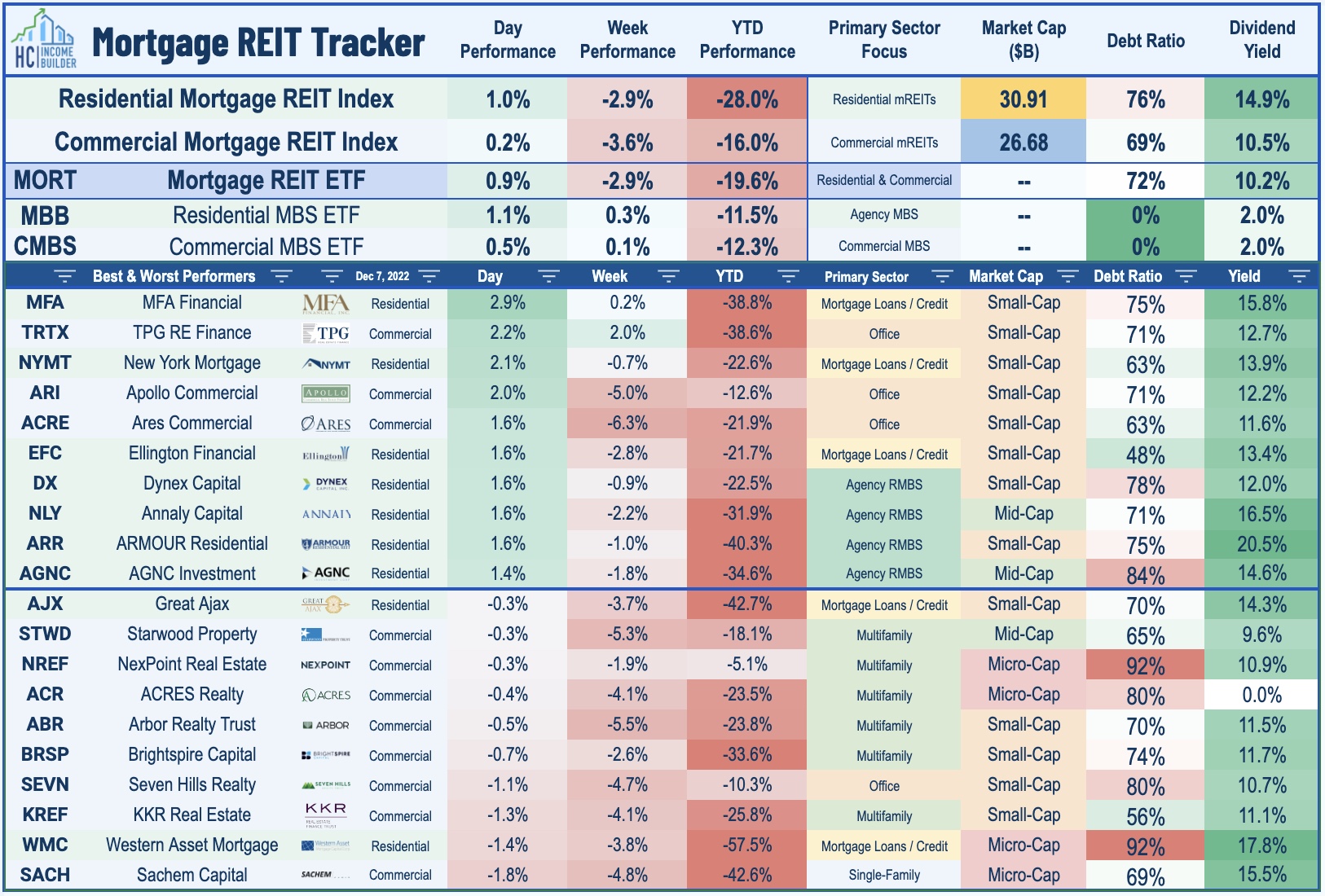

- Real estate equities were an area of strength today with the Equity REIT Index advancing 0.2% with 13-of-18 property sectors in positive territory while the Mortgage REIT Index gained 0.9%.

- Homebuilders and the broader Hoya Capital Housing Index rallied after stronger-than-expected results from luxury builder Toll Brothers and data showing that mortgage rates declined for a fourth-straight week.

- Self-storage REIT CubeSmart (CUBE) - which we own in the REIT Dividend Growth Portfolio - hiked its quarterly dividend by 14%. INDUS Realty (INDT) hiked its payout by 13%.

Income Builder Daily Recap

U.S. equity markets finished lower for a fifth-day Wednesday even as long-term interest rates dipped to three-month lows as investors weighed the risk of recession against encouraging news on the inflation front. Extending its declines to nearly 3.5% on the week, the S&P 500 dipped another 0.2% today while the Nasdaq 100 declined 0.4%. Real estate equities were an area of strength today with the Equity REIT Index advancing 0.2% with 13-of-18 property sectors in positive territory while the Mortgage REIT Index gained 0.9%. Homebuilders and the broader Hoya Capital Housing Index rallied after stronger-than-expected results from luxury builder Toll Brothers and data showing that mortgage rates declined for a fourth-straight week.

Another day, another encouraging inflation report. Data from the Labor Department this morning showed that Unit Labor Costs rose at just a 2.4% rate in the third quarter - lower than the initial estimate of 3.5% and down sharply from the double-digit rates seen in the first-half of 2022. The 10-Year Treasury Yield (US10Y) dipped another 11 basis points to close back at 3.41% - the lowest levels since mid-September. Crude Oil prices dipped another 2% today - now negative on a year-over-year basis - while Gasoline prices in the U.S. have also turned negative on a year-over-year basis and lower by over 35% from the peak in June. Four of the eleven GICS equity sectors were higher on the day with Healthcare (XLV) stocks leading on the upside while Consumer Discretionary (XLC) stocks lagged.

Real Estate Daily Recap

Best & Worst Performance Today Across the REIT Sector

Single-Family Rentals: Today we published Single Family Rental REITs: Save The Gloom & Doom on the Income Builder Marketplace which discussed our updated sector outlook and recent portfolio allocations. SFR REITs have uncharacteristically lagged - dipping by more than 30% this year - swept up by stiff headwinds across the housing industry from the historic surge in mortgage rates. Cooling home price appreciation and tightening credit conditions is indeed bad news for many new “start-up” entrants into the SFR scene that are learning the hard way that the SFR game is a capital-intensive business that requires significant scale to operate profitably. Despite the sharp rate-driven housing cooldown, household formations have actually accelerated this year, lifted by historic levels of inbound immigration and an uptick in birth rates - challenging two core tenants of housing skeptics' prognoses.

A trio of REITs hiked their dividends over the past 24 hours. CubeSmart (CUBE) - which we own in the REIT Dividend Growth Portfolio - hiked its quarterly dividend by 14% to $0.49/share. INDUS Realty Trust (INDT) - which soared last week on a proposed takeout at $65/share - hiked its quarterly dividend by 12.5% to $0.18 per share. Micro-cap Presidio Property Trust (SQFT) - which slashed its dividend earlier this year - raised its quarterly payout by 5% to $0.021/share - but still well below its $0.106/share rate before the cut. As noted in our State of the REIT Nation report last week, REIT payout ratio ratios remain below the long-term historical averages, implying that REITs have significant 'embedded' dividend growth that should be unlocked over the coming quarters - or at least serve as a buffer to protect current payout levels if macroeconomic conditions take an unfavorable turn.

Additional Daily REITBeat Headlines Available on Income Builder

- Income Builder Members receive access to The Daily REITBeat, an institutional-quality daily note that keeps subscribers apprised of pertinent news, data, and trends specifically within the REIT industry.

- Brandywine (BDN) priced $350 million of 7.55% guaranteed notes due 2027 and intends to use net proceeds of the offering to repurchase or redeem the $350 million outstanding principal amount of its 3.95% Guaranteed Notes due February 15, 2023 and for general corporate purposes, which may include the repayment, repurchase or other retirement of other indebtedness

- Armada Hoffler (AHH) announced a new $100 million unsecured term loan with the option to increase the total capacity to $200 million where proceeds from the term loan have been used to unencumber the company’s newly stabilized Wills Wharf asset, as well as three Town Center of Virginia Beach retail assets and the new term loan matures concurrently with the existing line in January 2027 at a fixed interest rate of 4.79%

- Farmland Partners (FPI) announced that it purchased a Texas farm for $12.1 million noting that the acquisition represents its first farmland transaction in the state since selling property there in 2020 as the new 3,843-acre site sits in Dallam and Hartley Counties in the northwest corner of Texas that primarily produces potatoes, in addition to corn and wheat

- Store Capital (STOR) announced that the Committee on Foreign Investment in the United States (CFIUS) has approved the previously announced all-cash acquisition of the Company by affiliates of GIC, a global institutional investor, and funds managed by Oak Street, a Division of Blue Owl noting that the transaction is expected to close in the first quarter of 2023

- Outfront Media (OUT) announced that its subsidiary, Outfront Media Canada LP acquired 57 static posters and 24 digital billboard assets in St. John's, Newfoundland and Labrador, Canada from Digital Outdoor Media Inc., or DOMI (formerly known as E.C. Boone Ltd.) funded using cash on hand

Mortgage REIT Daily Recap

Per the REIT Rankings Tracker available to Income Builder subscribers, mortgage REITs rebounded today with residential mREITs advancing 1.0% while commercial mREITs gained 0.2%. PennyMac Mortgage (PMT) advanced 1.4% today after confirming its prior indication that it would be reducing its dividend by 15% to $0.40/share which reflects its "objective to distribute its income that reflects the earnings per share we expect from our current investment strategies." In Mortgage REITs: High Yields Are Fine, For Now, PMT was one of several mREITs that we flagged as likely to reduce its distribution. Despite paying average dividend yields in the mid-teens, the majority of mREITs have been able to cover their dividends as improved earnings power from wider investment spreads offset book value declines.

Economic Data This Week

The economic calendar slows down this week, headlined by the Producer Price Index on Friday which investors - and the Fed - are hoping to show that the fastest pace of year-over-year increases is finally behind us. The headline PPI is expected to moderate to a 7.2% year-over-year rate while the Core PPI is expected to decelerate slightly to 5.9%. On Friday, we'll also get our first look at Michigan Consumer Sentiment for December. The Fed is particularly interested in the 5-Year Inflation Expectations survey, looking for signs of a potential "wage-price inflation spiral" through elevated consumer wage expectations. We'll also see a handful of Purchasing Managers Index ("PMI") reports throughout the week from S&P Global and the Institute for Supply Management. Both of these major surveys posted readings below the breakeven-50 level in their preliminary November data.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital Research & Index Innovations (“Hoya Capital”) is an affiliate of Hoya Capital Real Estate, a registered investment advisory firm based in Rowayton, Connecticut that provides investment advisory services to ETFs, individuals, and institutions. Hoya Capital Research & Index Innovations provides non-advisory services including market commentary, research, and index administration focused on publicly traded securities in the real estate industry.

This published commentary is for informational and educational purposes only. Nothing on this site nor any commentary published by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. This commentary is impersonal and should not be considered a recommendation that any particular security, portfolio of securities, or investment strategy is suitable for any specific individual, nor should it be viewed as a solicitation or offer for any advisory service offered by Hoya Capital Real Estate. Please consult with your investment, tax, or legal adviser regarding your individual circumstances before investing.

The views and opinions in all published commentary are as of the date of publication and are subject to change without notice. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Any market data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any outlook made in this commentary will be realized.

Readers should understand that investing involves risk and loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks, as do investments in ETFs. The information presented does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes.

Hoya Capital Real Estate and Hoya Capital Research & Index Innovations have no business relationship with any company discussed or mentioned and never receives compensation from any company discussed or mentioned. Hoya Capital Real Estate, its affiliates, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings and additional important disclosures is available at www.HoyaCapital.com.