Amazon Layoffs • Rents Decline • Payrolls Ahead

- U.S. equity markets finished lower Thursday as employment data from ADP and the DOL showed evidence of continued strength in labor markets despite another wave of large-scale corporate layoff announcements.

- Dipping back into negative territory for the week, the S&P 500 slipped 1.3% today while the tech-heavy Nasdaq 100 dipped 1.6%. The 2-Year Treasury Yield jumped by the most in a month.

- After leading the gains in the first two sessions of 2023, real estate equities were among the laggards today. Equity REITs slipped 2.8% today while Mortgage REITs declined 0.5%.

- ADP reported today that private payrolls expanded by 235,000 in December - ahead of consensus estimates of 150k - and accelerating from the 182k jobs added in November.

- Apartment List's national index fell by 0.8% over the course of December, marking the fourth straight month-over-month decline. For the full-year, national median rent increased by a total of 3.8% - a notably sharp slowdown from the 17.6% surge in 2021.

Income Builder Daily Recap

U.S. equity markets finished lower Thursday as employment data from ADP and the DOL showed evidence of continued strength in labor markets despite another wave of large-scale corporate layoff announcements. Dipping back into negative territory for the week, the S&P 500 slipped 1.3% today while the tech-heavy Nasdaq 100 dipped 1.6%. After leading the gains in the first two sessions of 2023, real estate equities were among the laggards today with the Equity REIT Index slipping 2.8% today with all 18 property sectors in negative-territory while the Mortgage REIT Index declined 0.5%.

Ahead of the critical nonfarm payrolls report on Friday morning, bond markets snapped a two-day streak of gains after relatively strong ADP payrolls and jobless claims data weakened the case for an imminent Fed pivot towards less-aggressive tightening. The policy-sensitive 2-Year Treasury Yield (US2Y) climbed by the most in a month to 4.46% but the 10-Year Treasury Yield (US10Y) remained relatively stable at 3.72%. Crude Oil prices rebounded by 0.7% following two days of declines. Ten of the eleven GICS equity sectors were lower on the day with the yield-sensitive Real Estate (XLRE) and Utilities (XLU) lagging while technology stocks were also under pressure following an announcement from Amazon (AMZN) that it plans to layoff more than 18,000 employees, citing a weakening economic outlook.

U.S. labor markets have been one of the few remaining "holdouts" in showing evidence of slowing economic growth. ADP reported today that private payrolls expanded by 235,000 in December - ahead of consensus estimates of 150k - and accelerating from the 182k jobs added in November. Notably, ADP reported that large companies (500+ employees) shed 151k jobs for the month, but relatively strong hiring among small and mid-sized businesses - particularly in the services sectors - more-than-offset these corporate layoffs. In a separate report, the DOL reported that Initial Jobless Claims declined to 204k last week - the least since September - while Continuing Claims ticked down to 1.694 million after hitting the highest-levels since February.

Real Estate Daily Recap

Best & Worst Performance Today Across the REIT Sector

Apartments: Residential REITs were in focus today after data from Apartment List showed that multifamily rents continued to decline in December - continuing a trend of moderation since peaking at double-digit annual percentage increases in mid-2022. Apartment List's national index fell by 0.8% over the course of December, marking the fourth straight month-over-month decline. The firm commented that "the timing of this cooldown in the rental market is consistent with the typical seasonal trend, but its magnitude has been notably sharper than what we’ve seen in the past." For the full-year, national median rent increased by a total of 3.8% - a notably sharp slowdown from the 17.6% surge in rents that we saw in 2021. Rent growth in 2022 still ranked as the second fastest year in Apartment Lists' records. Rents decreased in December in 90 of the nation’s 100 largest cities with New York City recording the nation’s sharpest monthly decline.

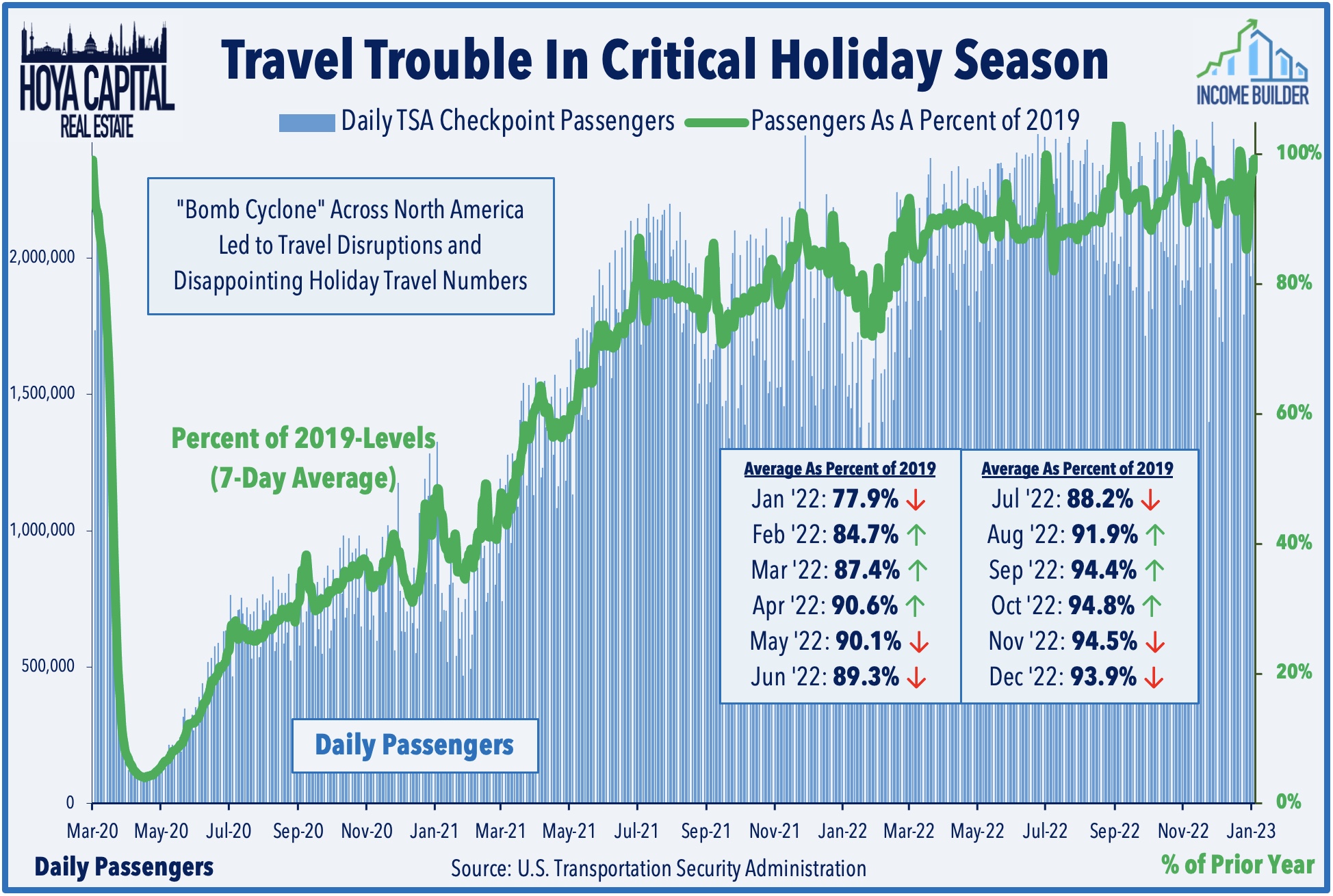

Hotels: Hospitality stocks have also been in focus this week as investors parsed the impacts of the weather-related disruptions during the critical holiday travel season. Recent TSA checkpoint data shows that passenger-throughout finished the holiday season relatively strong around the New Year Holiday with the 30-Day average hovering around 99% of pre-pandemic levels. In REIT news, Host Resorts (HST) announced today that it amended and restated its existing $2.5 billion credit facility which extends maturities from January 2025 to January 2028, including all extension options, and continues to provide a $1.5 billion revolving credit facility and two $500 million term loans plus also reflects the Company’s industry-leading commitment to ESG initiatives by adding incentives linked to portfolio sustainability initiatives, including green building certifications and renewable electricity usage.

Additional Headlines from The Daily REITBeat on Income Builder

- Healthcare Realty (HR) announced the completion of $1.14 billion of asset sales and joint venture contributions since July 2022 at a 4.86% cap rate generating net proceeds of $1.03 billion.

- Agree Realty (ADC) announced that acquisition volume for the fourth quarter totaled $404.9 million at a weighted-average capitalization rate of 6.4% and had a weighted-average remaining lease term of 10.6 years.

- Rexford (REXR) announced the acquisition of ten industrial properties for $336.2 million which were funded using a combination of cash on hand and proceeds from forward equity settlements.

- Plymouth (PLYM) announced fourth quarter leasing volume totaled 2.3M sf and achieved a 18.1% blended cash rental rate spread.

- We're excited to announce that Armada ETF Advisors is a new contributing author on Income Builder. Members now receive access to Armada's insights and analysis focused on residential REITs.

Mortgage REIT Daily Recap

Per the REIT Rankings Tracker available to Income Builder subscribers, mortgage REITs were mixed today with residential mREITs advancing 0.1% while commercial mREITs slipped 0.5%. On a quiet day of newsflow in the mREIT space, notable leaders included Ellington Residential (EARN) and PennyMac (PMT) while iStar (STAR) and NexPoint Real Estate (NREF) were laggards. Last month, we published Mortgage REITs: High Yields Are Fine, For Now, which noted that despite paying average dividend yields in the mid-teens, the majority of mREITs have been able to cover their dividends, but we flagged a handful of mREITs with payout ratios above 100% of EPS.

Economic Data This Week

As noted in our Real Estate Weekly Outlook, employment data highlights a holiday-shortened week of economic data this week, concluding on Friday with the BLS Nonfarm Payrolls report. Economists are looking for job growth of roughly 200k in December - which would be the smallest gain since December 2020 - and for the unemployment rate to stay steady at 3.7%. 'Good news is bad news' will likely be the theme of these reports as investors and the Fed await the long-awaited cooldown in labor markets which has yet to fully materialize. Strong job gains observed in the BLS' nonfarm establishment survey, however, have been at odds with most other employment metrics showing a more material slowdown in hiring including the BLS' household survey in the same report which showed a second-straight month of net job declines last month.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital Research & Index Innovations (“Hoya Capital”) is an affiliate of Hoya Capital Real Estate, a registered investment advisory firm based in Rowayton, Connecticut that provides investment advisory services to ETFs, individuals, and institutions. Hoya Capital Research & Index Innovations provides non-advisory services including market commentary, research, and index administration focused on publicly traded securities in the real estate industry.

This published commentary is for informational and educational purposes only. Nothing on this site nor any commentary published by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. This commentary is impersonal and should not be considered a recommendation that any particular security, portfolio of securities, or investment strategy is suitable for any specific individual, nor should it be viewed as a solicitation or offer for any advisory service offered by Hoya Capital Real Estate. Please consult with your investment, tax, or legal adviser regarding your individual circumstances before investing.

The views and opinions in all published commentary are as of the date of publication and are subject to change without notice. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Any market data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any outlook made in this commentary will be realized.

Readers should understand that investing involves risk and loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks, as do investments in ETFs. The information presented does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes.

Hoya Capital Real Estate and Hoya Capital Research & Index Innovations have no business relationship with any company discussed or mentioned and never receives compensation from any company discussed or mentioned. Hoya Capital Real Estate, its affiliates, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings and additional important disclosures is available at www.HoyaCapital.com.