CPI Ahead • Travel Trouble • REITs Lead Rebound

- U.S. equity markets rallied Wednesday while benchmark interest rates retreated as investors took positions ahead of the critical CPI inflation report which will dictate the near-term direction of monetary policy.

- Pushing its week-to-date gains to nearly 2%, the S&P 500 climbed 1.3% today while the tech-heavy Nasdaq 100 rallied 1.7%.

- Real estate equities - perhaps the most significant potential beneficiaries of an easing of inflation and interest rate pressures - were among the leaders today.

- Hotel REITs were among the leaders today despite the FAA-related travel disruptions. DiamondRock (DRH) rallied 5% after reporting preliminary fourth-quarter operating metrics, noting that its Revenue Per Available Room ("RevPAR") was 6.1% above the comparable pre-pandemic period in 2019.

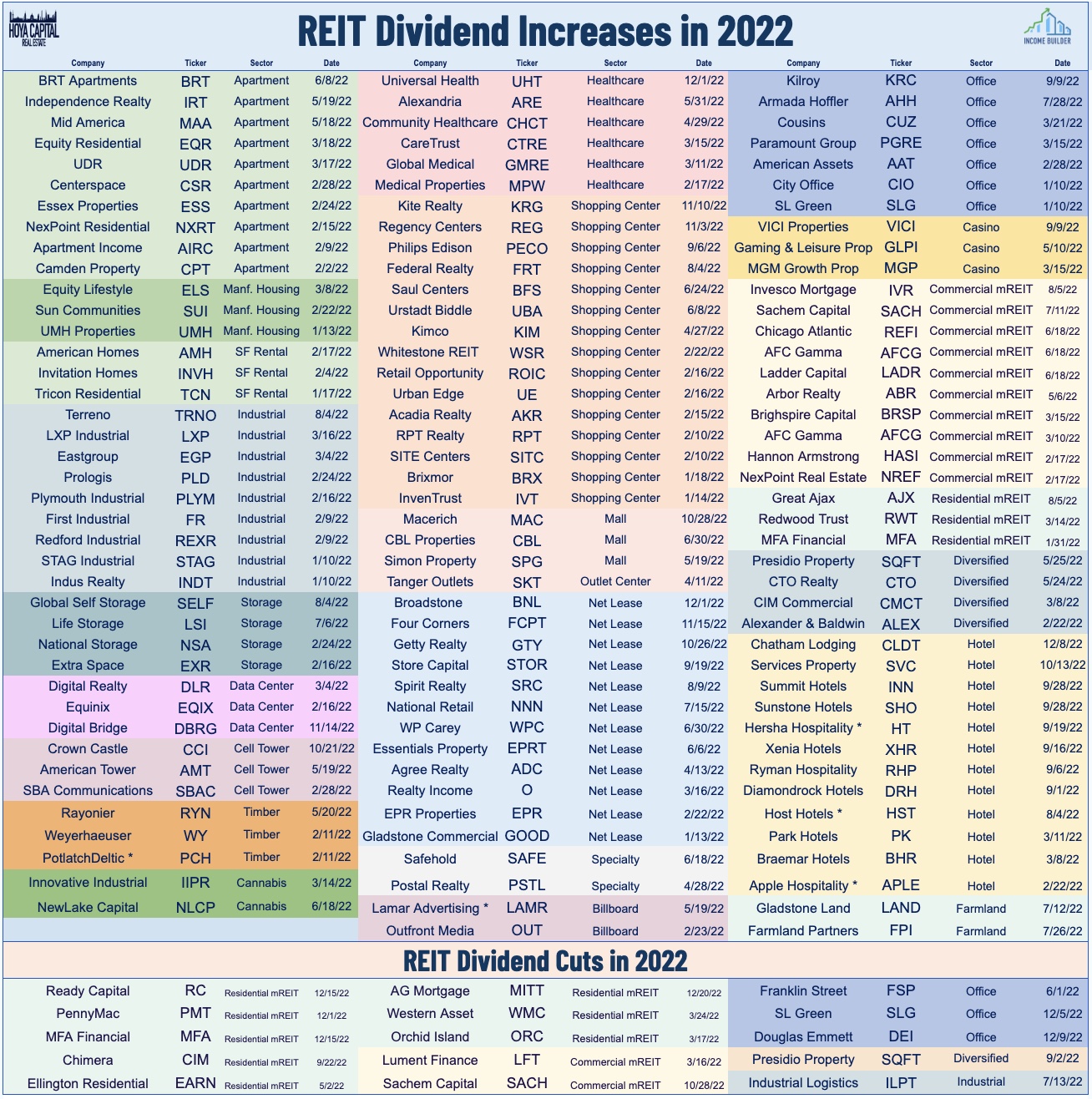

- Gladstone Commercial (GOOD) slid more than 13% today after it announced that it will reduce its monthly dividend from $0.1254 to $0.10 per share "in an effort to increase retained capital in anticipation of further economic headwinds."

Income Builder Daily Recap

U.S. equity markets rallied Wednesday while benchmark interest rates retreated as investors took positions ahead of the critical CPI inflation report which will dictate the near-term direction of monetary policy. Pushing its week-to-date gains to nearly 2%, the S&P 500 climbed 1.3% today while the tech-heavy Nasdaq 100 rallied 1.7%. Real estate equities - perhaps the most significant potential beneficiaries of an easing of inflation and interest rate pressures - were among the leaders today. The Equity REIT Index rallied 3.6% with all 18 property sectors in positive territory while the Mortgage REIT Index advanced 1.9%. Homebuilders and the broader Hoya Capital Housing Index gained nearly 3%, buoyed by mortgage market data showing a modest rebound in demand alongside a continued retreat in mortgage rates.

Bonds rallied as well today ahead of the key CPI inflation report tomorrow morning as the 10-Year Treasury Yield dipped 7 basis points to close at 3.55% - back on the cusp of the lowest-levels since September and well below its peak closing high of 4.25% in October. The headline CPI is expected to moderate to a 6.5% year-over-year rate while the Core CPI is expected to decelerate to 5.7%. All eleven GICS equity sectors were higher today with the yield-sensitive segments leading on the upside. Travel stocks lagged after the FAA was forced to issue a nationwide grounding of aircraft due to technical malfunctions that interfered with key safety information systems.

Real Estate Daily Recap

Best & Worst Performance Today Across the REIT Sector

Hotel: Hotel REITs were among the leaders today despite the FAA-related travel disruptions. Diamondback (DRH) rallied 5% after reporting preliminary fourth-quarter operating metrics, noting that its Revenue Per Available Room ("RevPAR") was 6.1% above the comparable pre-pandemic period in 2019. For the full-year, DHR recorded RevPAR growth of 5.0% above 2019-levels. Consistent with the trend seen across the hotel sector, DRH recorded very strong performance in its leisure-oriented Resort portfolio - which generated comparable RevPAR growth of 18% above pre-pandemic levels in Q4 - but its business-oriented Urban portfolio remained 2% below pre-pandemic RevPAR levels. Elsewhere, Xenia Hotels (XHR) announced that it has successfully obtained a new $675M senior unsecured credit facility. Recent TSA checkpoint data shows that passenger throughput finished the holiday season relatively strong around the New Year Holiday and into early 2023. The first week of January saw throughput levels that were 5% above pre-pandemic levels.

Manufactured Housing: After the close today, UMH Properties (UMH) - which we own in the REIT Focused Income Portfolio - raised its quarterly dividend by 2.5% to $0.205/share. Yesterday we published Manufactured Housing: Recession Resistant REITs. MH REITs snapped an incredible streak of nine straight years of outperformance over the REIT Index in 2022, impacted by headwinds from higher interest rates and hurricane-related disruptions. While rent growth has moderated from record-high levels across other residential property types, MH revenue growth is poised to accelerate in 2023, driven by their under-appreciated inflation-linkage and Cost-of-Living-Adjustment effects. Nearly half of MH residents receive monthly Social Security benefits, which are poised to rise 8.7% beginning this month - the highest COLA increase in four decades - which will give MH REITs and senior housing REITs room to push rent growth.

Net Lease: Gladstone Commercial (GOOD) slid more than 13% today after it announced that it will reduce its monthly dividend from $0.1254 to $0.10 per share "in an effort to increase retained capital in anticipation of further economic headwinds." GOOD had been one of just a dozen REITs to deliver dividend increases in each of the pandemic years, hiking its cumulative annual payout by about 1% in 2020, 2021, and 2022. GOOD announced that its external advisor will waive the incentive fee for the quarters ending March 31, 2023 and June 30, 2023. Buzz Cooper, the company's President, stated, "We believe that the dividend cut, along with the temporary incentive fee waiver, will help the Company to maintain a strong balance sheet in 2023."

Additional Headlines from The Daily REITBeat on Income Builder

- Truist Securities upgraded Gaming & Leisure Properties (GLPI) to Buy from Hold.

- BTIG downgraded Elme Communities (ELME), and Equity Residential (EQR) and Retail Opportunities (ROIC) to Neutral from Buy.

Mortgage REIT Daily Recap

Per the REIT Rankings Tracker available to Income Builder subscribers, mortgage REITs continued their strong start to the year with residential mREITs gaining another 2.2% today while commercial mREITs also gained 2.2%. Redwood Trust (RWT) gained 3.5% today after it launched a new $65M preferred issue, pricing 2.6M shares of 10.00% Series A Fixed-Rate Reset Cumulative Redeemable Preferred Stock which will trade on the NYSE under symbol "RWT PRA" beginning next week. After the close today, AGNC Investment (AGNC) and Orchid Island (ORC) each held their dividends steady at current rates. Last month, we published Mortgage REITs: High Yields Are Fine, For Now, which noted that despite paying average dividend yields in the mid-teens, the majority of mREITs have been able to cover their dividends, but we flagged a handful of mREITs with payout ratios above 100% of EPS.

Economic Data This Week

It'll be another busy week of economic data with the main event coming on Thursday with the Consumer Price Index for December, which investors and the Fed are hoping will show that the fastest pace of year-over-year increases in inflation is finally behind us. The headline CPI is expected to moderate to a 6.5% year-over-year rate while the Core CPI is expected to decelerate to 5.7%. As with recent months, the metric we're watching most closely is the CPI-ex-Shelter Index - which since July has averaged a -1.9% annualized rate - among the most deflationary five-month periods on record. Critically, gasoline prices averaged $3.21 nationally in December - down about 13% from the prior month and 3% from the prior year. We'll also get our first look at Michigan Consumer Sentiment data on Friday - which includes a closely-watched consumer inflation expectations survey - and we'll be closely watching Jobless Claims data on Thursday as well.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital Research & Index Innovations (“Hoya Capital”) is an affiliate of Hoya Capital Real Estate, a registered investment advisory firm based in Rowayton, Connecticut that provides investment advisory services to ETFs, individuals, and institutions. Hoya Capital Research & Index Innovations provides non-advisory services including market commentary, research, and index administration focused on publicly traded securities in the real estate industry.

This published commentary is for informational and educational purposes only. Nothing on this site nor any commentary published by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. This commentary is impersonal and should not be considered a recommendation that any particular security, portfolio of securities, or investment strategy is suitable for any specific individual, nor should it be viewed as a solicitation or offer for any advisory service offered by Hoya Capital Real Estate. Please consult with your investment, tax, or legal adviser regarding your individual circumstances before investing.

The views and opinions in all published commentary are as of the date of publication and are subject to change without notice. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Any market data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any outlook made in this commentary will be realized.

Readers should understand that investing involves risk and loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks, as do investments in ETFs. The information presented does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes.

Hoya Capital Real Estate and Hoya Capital Research & Index Innovations have no business relationship with any company discussed or mentioned and never receives compensation from any company discussed or mentioned. Hoya Capital Real Estate, its affiliates, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings and additional important disclosures is available at www.HoyaCapital.com.