5G Cooldown? • REIT Earnings • Rally Fades

U.S. equity markets slumped Thursday while benchmark interest rates jumped as investors weighed surprisingly strong employment data and sluggish earnings reports from several large-cap technology stocks.

Retreating from its highest close since January 2022, the S&P 500 slipped 0.7% today, while the tech-heavy Nasdaq 100 dipped more than 2%.The Dow, however, posted a ninth-straight daily advance.

Real estate equities finished mostly lower today as the initial wave of earnings results from industrial and technology REITs has been modesty disappointing. The Equity REIT Index slipped 0.3%.

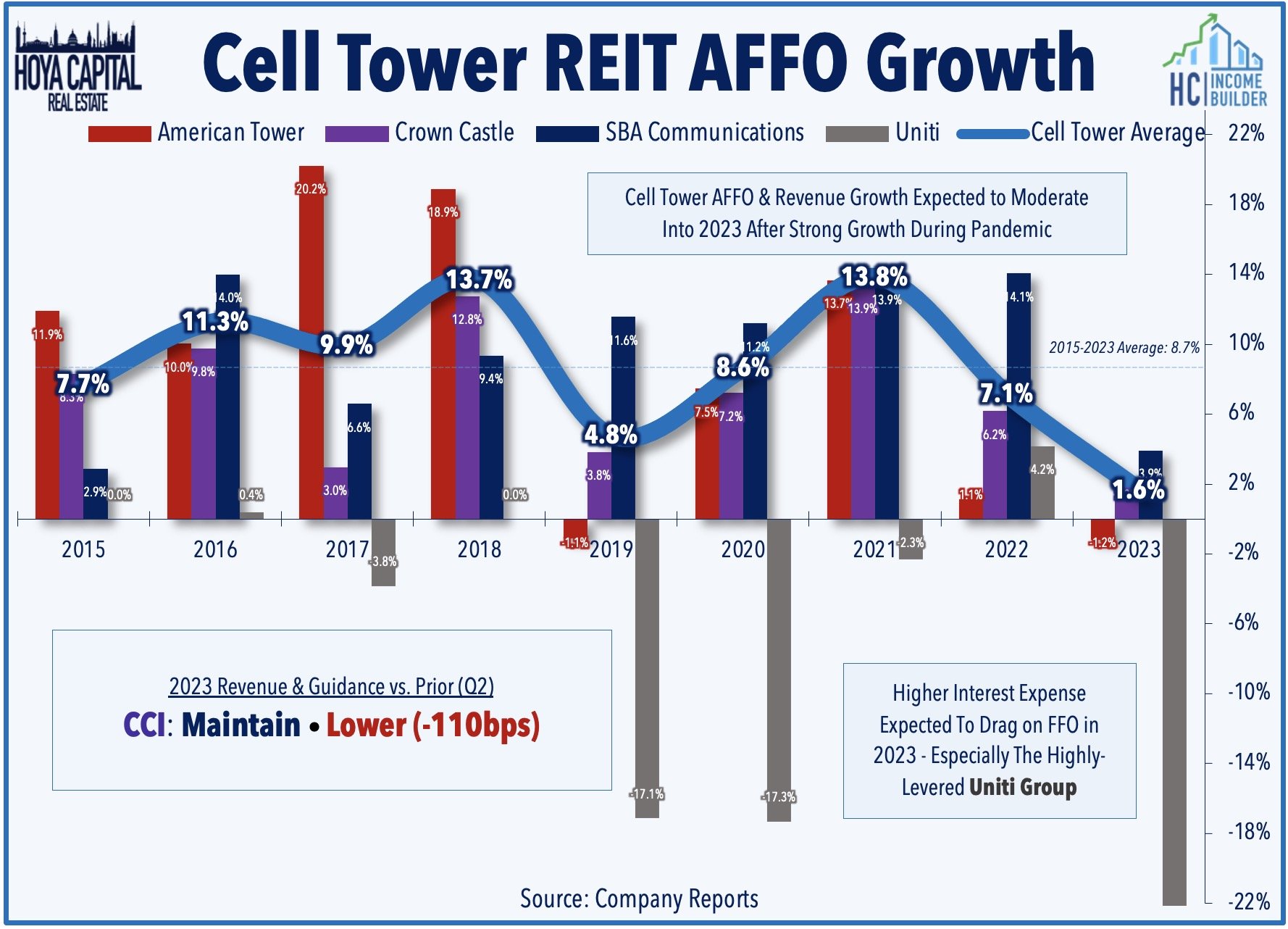

Cell tower REIT Crown Castle (CCI) dipped 5% today after reporting soft second-quarter results and lowered its full-year adjusted FFO outlook citing a "significant" slowdown in carrier network spending.

NYC-focused SL Green (SLG) dipped more 6% after its second-quarter results did little to alter the dire narrative enveloping coastal office properties.

Income Builder Daily Recap

U.S. equity markets slumped Thursday while benchmark interest rates jumped as investors weighed surprisingly strong employment data and sluggish earnings reports from several large-cap technology stocks. Retreating from its highest close since January 2022, the S&P 500 slipped 0.7% today, while the tech-heavy Nasdaq 100 dipped over 2%. The Dow, however, managed to advance for a ninth-straight session. Real estate equities finished mostly lower today as the initial wave of earnings results from industrial and technology REITs has been modesty disappointing. The Equity REIT Index slipped 0.3% today, but 11-of-18 property sectors finished in positive territory, while the Mortgage REIT Index declined 1.5%. The red-hot homebuilders slumped more than 4% despite a very strong report and upward guidance boost from DR Horton - the nation's largest builder - which reported a 37% year-over-year increase in net orders and far-exceeding EPS and revenue estimates.

Cell Tower: Crown Castle (CCI) dipped 5% today after reporting soft second-quarter results and lowered its full-year adjusted FFO outlook citing a "significant" slowdown in carrier network spending. CCI now expects its full-year FFO to rise 1.9% this year - a 110 basis point decrease from its prior outlook of 3.0% growth - but maintained its guidance ranges for revenues, adjusted EBITDA, and same-store property revenues. Industry-level commentary was surprisingly downbeat, with CCI noting that "the initial surge in tower activity [related to the 5G rollout] has ended," which led to a decline in tower activity (equipment upgrades and modifications) of more than 50% in the second-quarter. On the impacts of the recent WSJ reporting on potential remediation costs for AT&T and Verizon of old abandoned lead-containing network cables, CCI commented that it has "not seen any behavior change from our carrier customers... but obviously, they’re very healthy and have a long history of being able to navigate through various cycles."

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds ("ETFs") listed on the NYSE. In addition to any long positions listed, Hoya Capital is long all components in the Hoya Capital Housing Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital Research & Index Innovations (“Hoya Capital”) is an affiliate of Hoya Capital Real Estate, a registered investment advisory firm based in Rowayton, Connecticut that provides investment advisory services to ETFs, individuals, and institutions. Hoya Capital Research & Index Innovations provides non-advisory services including market commentary, research, and index administration focused on publicly traded securities in the real estate industry.

This published commentary is for informational and educational purposes only. Nothing on this site nor any commentary published by Hoya Capital is intended to be investment, tax, or legal advice or an offer to buy or sell securities. This commentary is impersonal and should not be considered a recommendation that any particular security, portfolio of securities, or investment strategy is suitable for any specific individual, nor should it be viewed as a solicitation or offer for any advisory service offered by Hoya Capital Real Estate. Please consult with your investment, tax, or legal adviser regarding your individual circumstances before investing.

The views and opinions in all published commentary are as of the date of publication and are subject to change without notice. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. Any market data quoted represents past performance, which is no guarantee of future results. There is no guarantee that any historical trend illustrated herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. There is no guarantee that any outlook made in this commentary will be realized.

Readers should understand that investing involves risk and loss of principal is possible. Investments in real estate companies and/or housing industry companies involve unique risks, as do investments in ETFs. The information presented does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. An investor cannot invest directly in an index and index performance does not reflect the deduction of any fees, expenses or taxes.

Hoya Capital Real Estate and Hoya Capital Research & Index Innovations have no business relationship with any company discussed or mentioned and never receives compensation from any company discussed or mentioned. Hoya Capital Real Estate, its affiliates, and/or its clients and/or its employees may hold positions in securities or funds discussed on this website and our published commentary. A complete list of holdings and additional important disclosures is available at www.HoyaCapital.com.